- Share:

Mortgage Services

A new property mortgage is a special type of loan granted to individuals or companies buying a new property for the first time. New property mortgages vary in tenure to suit you, ranging from 10 to 30 years. If you are looking for the best instalment to buy a new home, regardless of whether you have a previous property purchase, Lets Move Group's finance team can help.

Our new property mortgage service is able to provide you with competitive rates, the best lending options from our partners, and comprehensive assistance to ensure your property purchase process runs smoothly and efficiently.

Whether you are looking to own a home or expand your business in Indonesia, Lets Move Group will help you through the entire journey of applying for the best mortgage instalment scheme.

We offer a range of customised services for individuals seeking property and mortgage financing in Indonesia with the best tenure and instalment scheme for you. Our professional team of experts help provide solutions that suit your individual needs, providing the best interest rates and mortgage terms. Our goal is to provide the best property-buying experience in Indonesia.

Lets Move Group has partnered with Indonesia's most popular banks and financing institutions, including Bank Mandiri, BCA, Commonwealth, Panin, DBS, and Permata, just to name a few. We only work with trusted and professional banks so you can feel confident when dealing with a lender.

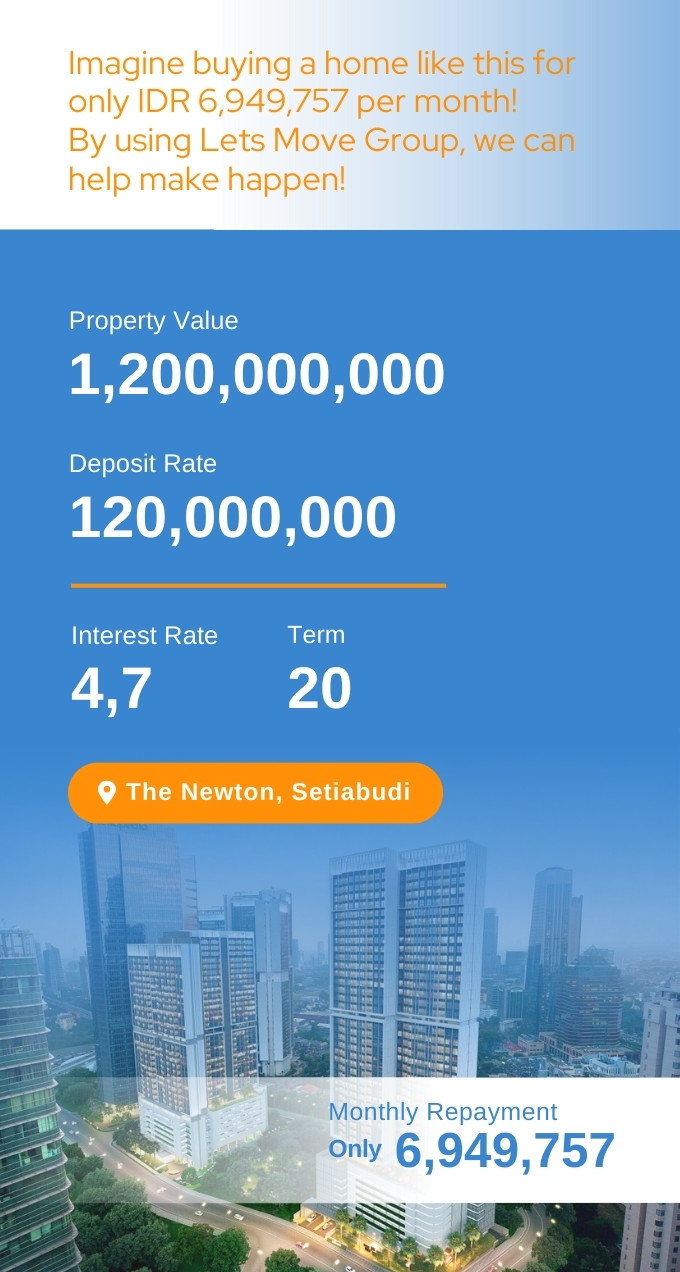

Most Indonesian banks can provide KPR starting from IDR 500 million. However, some banks can even provide mortgages starting from IDR 100 million.

In general, it takes five to fourteen working days to process a mortgage to completion, but it can take a few working days longer than expected if the bank requires further documents for the application.

To get a mortgage, you have to go through a data verification process and individual interviews. For more details on each process, you can speak to our financial advisors.

The longest mortgage loan period in Indonesia is up to 30 years. However, this depends on the age of the borrower when they complete the loan. The maximum age for debtors is 57 years old for employees, and 70 years old for self-employed individuals or entrepreneurs.

Yes, you pay additional costs such as Provision Fee, Administration Fee, Credit Life Insurance (one-time premium), Fire Insurance (one-time premium), Valuation Fee (if required), and Notary Fee. These fees above are subject to change at any time according to the bank's policy with prior notice to the customer.

These fees above are subject to change at any time in accordance with the bank's policy with prior notice to the customer.

Yes, you can make overpayments to shorten your mortgage term or reduce your overall loan principal. With that said, overpayments will incur a penalty fee of between 1-3% of the amount you pay. Therefore, if you need advice on overpayments, please do not hesitate to contact us.

Our journey started in 2016 with the sole aim of becoming the most ethical property and real estate agent in Indonesia. Our dream is to be a complete solution for the needs of expatriates, offering comprehensive solutions for property investment in Indonesia. Find Out More »

Enter your email address to get the latest updates and offers.

Copyright © Lets Move Group 2024.

Lets Move Group

Rate information

Interest rate is 4.7% fixed for the first 3 years, after that, the rate will move to a floating rate (currently 11%)

Requirements

General Personal Requirements

*Disclaimer